589 documented use cases.

Static hosting is enough.

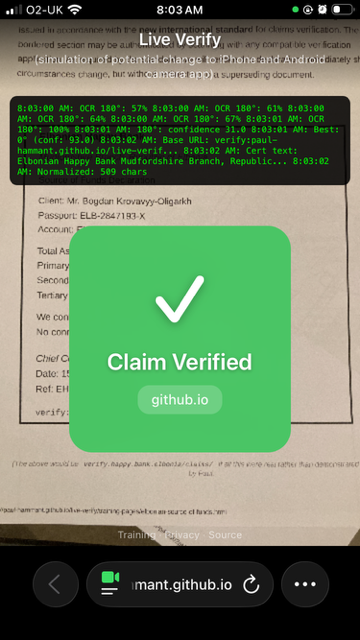

Live Verify: the next logical step up from the iPhone's Live Text.

Billions of smartphones already have OCR built-in via iOS Live Text and Android’s Camera Text features. A verification layer is the missing piece that upgrades those platforms into instant trust engines for physical documents—without blockchain, without apps, without QR codes.

The upside, without a new gatekeeper

This is a “trust primitive” for the physical world: readable claims (paper or screenshots) become machine-checkable without changing how people read documents. It improves verification without creating a single global gatekeeper or a mass-surveillance default.

Issuers keep authority by publishing from their own domains; verifiers decide what they trust; privacy remains on-device by default; and fraud detection becomes a familiar camera overlay, not a new workflow.

It’s also inclusive: it works with paper, screenshots, and low-end printers—no NFC chips, special ink, or new hardware required (though screens can introduce moiré patterns that demand higher-capability OCR). And it’s resilient: hashes can be published cheaply (even static hosting) while sensitive source records stay protected; verification can keep working during partial outages.

Market Scope

Every printed document that needs verification becomes instantly verifiable:

From immigration documents at borders to supply chain certifications at ports—589 documented use cases spanning every major industry.

Why Now?

Apple and Google are the natural distribution channel. Their camera apps already do OCR. Adding issuer-attested verification is an incremental step, and “Verified / Denied” is a natural camera overlay.

This is a camera feature, not a blockchain feature. “Live Text” graduated from third-party apps into the native camera experience; issuer-attested verification can follow the same path.

The question isn’t only if/when the platforms ship the UX—it’s whether there’s issuer infrastructure ready for them to query.

And the timing is forced from the other side. Generative AI made visually perfect forgery effectively free—anyone can produce a pixel-perfect bank statement or test report in seconds. Detection is an arms race defenders lose; issuer attestation is not. When a platform ships the "is this real?" gesture, what it delivers isn't a yes/no—it's a jurisdictional reveal: who stands behind the document or the person in front of you, the human reading the domain and the device walking the authority chain to a sovereign root in the same instant (dual-channel trust). The floor is a hash lookup; the ceiling—rotating-salt burn-on-verify badges that make a photographed credential worthless seconds later—is real-world physical-safety infrastructure.

The Window

Platforms may offer commodity storage of hashes, but integration is the hard part. There’s room for a company with sophisticated integration into existing commercial, organizational, and government systems to become the preferred “issuer registry + integrations” layer.

Focus on deep integration, compliance, and being the partner that institutions trust for publication, revocation, auditability, and uptime—even if the camera UX becomes commoditized.

This has a recent historical precedent: Let's Encrypt commoditized paid TLS certificates within a decade, funded by companies whose businesses grew when verification became ambient — and the durable commercial value moved up-stack to management and operations. The full episode, including who backed it and how incumbents reacted, is examined in Let's Encrypt as precedent.

Commercial path (SaaS)

The protocol is intentionally simple and not patent-locked — in fact unpatentable by anyone, having been publicly disclosed as prior art in January 2023. Defensibility comes from execution: integrations, governance, and trust.

Issuer Registry SaaS: publish hashes from systems of record, handle revocations, provide response-code meaning pages, and meet compliance/audit expectations.

Verifier Ops SaaS: managed app/SDK, device management, allowlists of issuer domains, optional caching and logging/retention controls (where authorized).

Explore the full catalog at /use-cases/ to see the breadth across industries.

Technical Foundation

This isn't vaporware. The proof-of-concept demonstrates the complete flow:

✓ Client-side OCR (privacy-preserving)

✓ SHA-256 hashing with normalization

✓ Domain-binding for issuer verification

✓ Works with existing infrastructure—at the most inexpensive end this can even be a static web server (no login required to serve the hash files)

What remains is production hardening and reliability: ornate typography and screens can introduce OCR challenges (including moiré patterns), and this prototype uses browser-based OCR. Platform-grade on-device OCR (or native apps) can improve the scan rate dramatically.

Where do you fit?

This page is the wide-angle view. The role-specific cases — with effort estimates, business cases, and a founding-adopter offer — are here:

For issuers (organizations whose documents get forged) · For SaaS builders (software that issues documents) · For platforms (camera, browser, OS, PDF vendors) · If you sell verification today (incumbents & investors) · Founding adopter program

Pilots, integrations, questions: paul@hammant.org (Paul Hammant)